Preprint Published on "A New Multi-agent Simulation Framework Powered by LLMs."

2025-11-19

- article

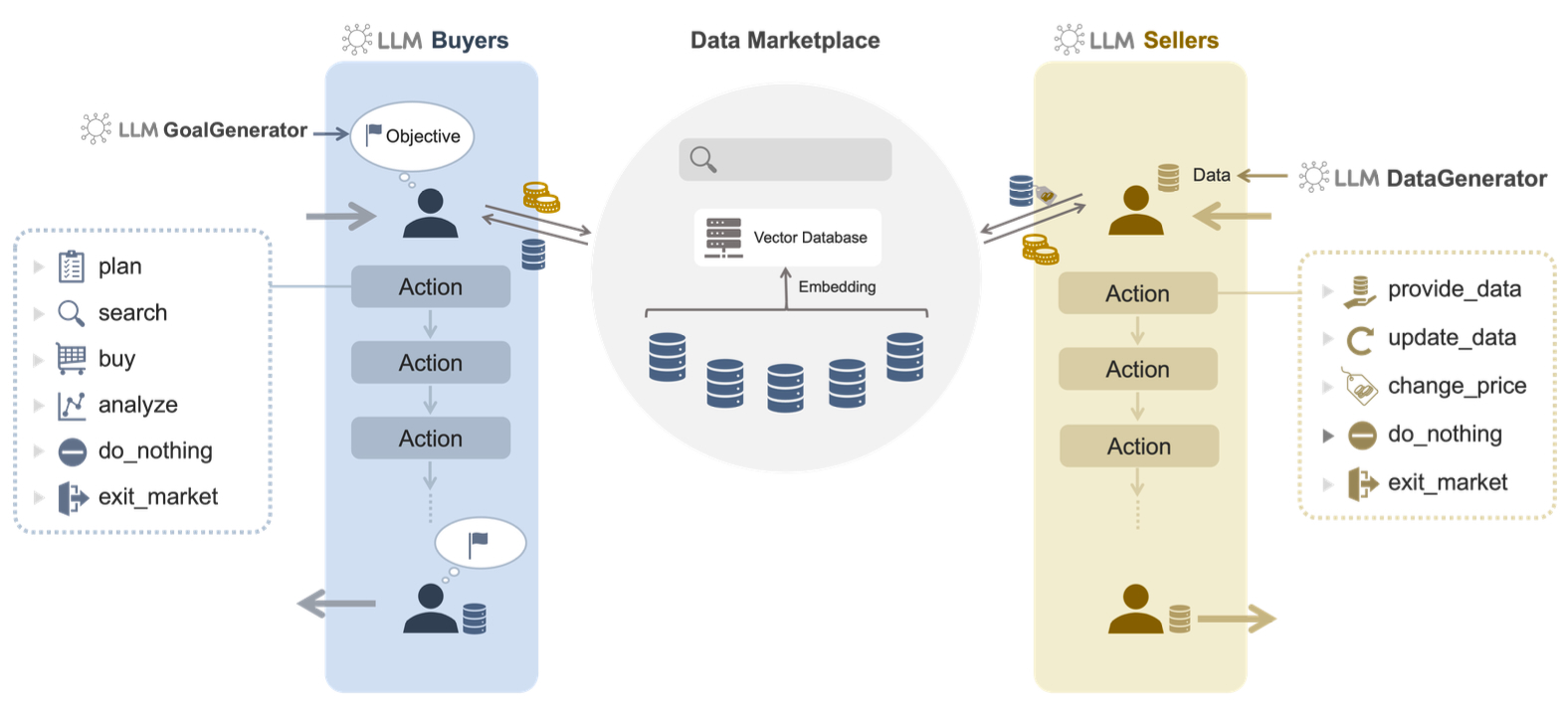

As data ecosystems continue to advance, data marketplaces—platforms that enable organizations to purchase and exchange datasets from third parties—are gaining attention as an important source of innovation. Yet, in real markets, we still lack a systematic understanding of what objectives buyers and sellers pursue, how they act strategically, and how these behaviors collectively shape market-wide dynamics. To address these challenges, this study proposes a new multi-agent simulation framework powered by Large Language Models (LLMs).

Traditional simulations of data marketplaces have largely relied on rule-based or model-based approaches, in which agent behaviors are predetermined and constrained. However, these approaches struggle to reproduce the complex decision-making observed in real markets—such as diverse objectives, context-dependent strategy changes, and adaptation to emerging market trends.

In contrast, our research constructs a system in which buyer and seller agents are each assigned natural-language “goals,” enabling them to autonomously choose actions such as data exploration, purchasing, pricing, and updating through LLM-driven reasoning. This design allows the simulation to capture behavioral patterns that are difficult to express in conventional rule-based models.

Through the simulation, we analyzed key characteristics of market structure—such as the number of transactions per dataset, purchasing patterns of individual buyers, and repeated purchases of the same dataset—and compared these with transaction records from the real data marketplace service. The results show that our framework successfully reproduces important market features, including the concentration of demand on specific datasets, the scale-free structure of buyer–seller networks, and the emergence of domain-specific trends. Notably, we also observed temporal shifts in demand toward particular fields, a phenomenon commonly seen in real data markets.

This study demonstrates how interactions among agents equipped with strategic intent and goal-oriented behavior can give rise to market-level structures and dynamics. Our long-term aim is to develop simulation tools that can support institutional design for future data marketplaces. As next steps, we plan to extend the framework to incorporate heterogeneous data types, more detailed modeling of post-purchase analysis behaviors, and mechanisms for information sharing and cooperation among multiple agents, advancing both the understanding and design of data markets.

https://arxiv.org/abs/2511.13233

Title: LLM-based Multi-Agent System for Simulating Strategic and Goal-Oriented Data Marketplaces

Authors: Jun Sashihara, Yukihisa Fujita, Kota Nakamura, Masahiro Kuwahara, Teruaki Hayashi

Abstract: Data marketplaces, which mediate the purchase and exchange of data from third parties, have attracted growing attention for reducing the cost and effort of data collection while enabling the trading of diverse datasets. However, a systematic understanding of the interactions between market participants, data, and regulations remains limited. To address this gap, we propose a Large Language Model-based Multi-Agent System (LLM-MAS) for data marketplaces. In our framework, buyer and seller agents powered by LLMs operate with explicit objectives and autonomously perform strategic actions, such as planning, searching, purchasing, pricing, and updating data. These agents can reason about market dynamics, forecast future demand, and adjust strategies accordingly. Unlike conventional model-based simulations, which are typically constrained to predefined rules, LLM-MAS supports broader and more adaptive behavior selection through natural language reasoning. We evaluated the framework via simulation experiments using three distribution-based metrics: (1) the number of purchases per dataset, (2) the number of purchases per buyer, and (3) the number of repeated purchases of the same dataset. The results demonstrate that LLM-MAS more faithfully reproduces trading patterns observed in real data marketplaces compared to traditional approaches, and further captures the emergence and evolution of market trends.